seagullsovergrimsby

#cpfctinpotclub

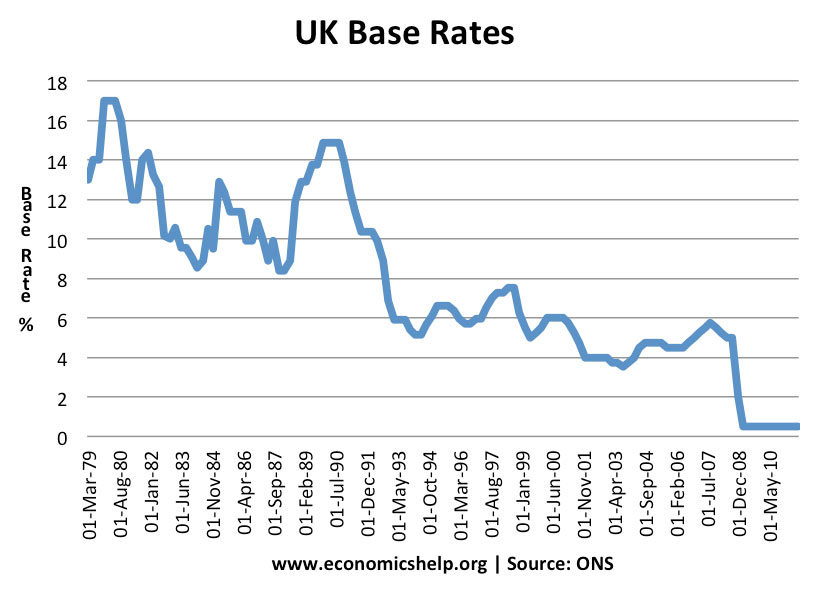

As I posted , the money men don't trust Labour but absolutely adore the Tories.Bank of England independent of Government, so rates will be determined by the global markets and BoE responses to our economy.

Then god forbid Moribund and Balls are given a second go at a government spending spree, either alone or in a coalition:

- rates would have to rise if a Balls borrowed spending spree led to inflation and/or global markets reacting badly to Labour's policies and their effects.